Setting the list price for your home involves evaluating various market conditions and financial factors. During this phase of the home selling process, your REALTOR® will help you set your list price based on:

- Pricing Considerations

- Comparable Sales

- Market Conditions

- Offering Incentives

- Estimated Net Proceeds

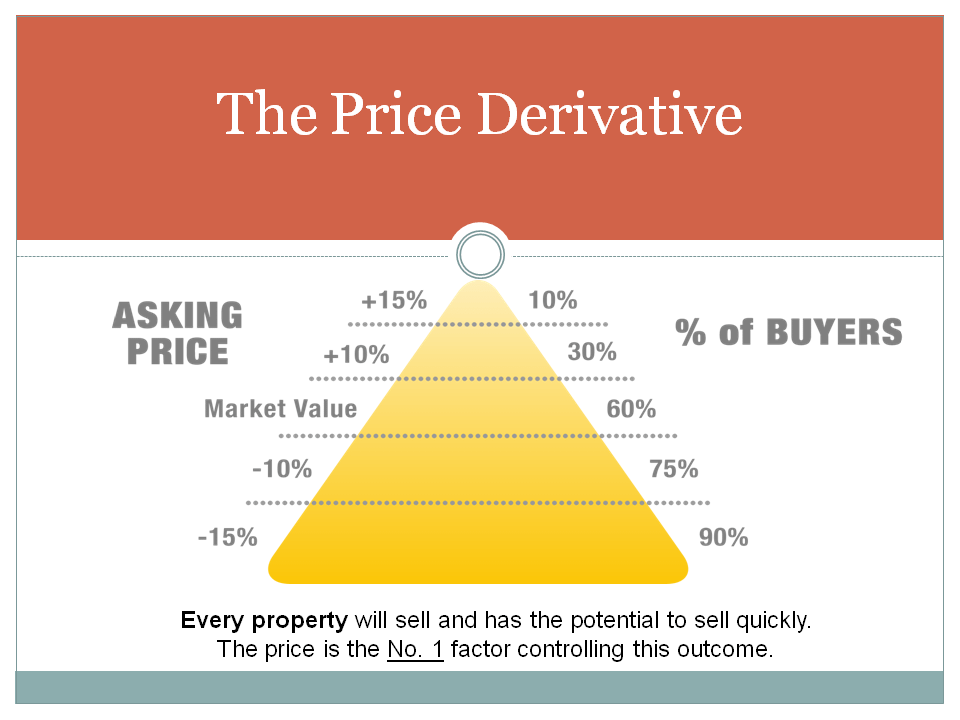

Pricing Considerations – Find a Balance Between Too High and Too Low

When setting a list price for your home, you should be aware of a buyer’s frame of mind. Consider the following pricing factors:

If you set the price too high, your house won’t be picked for viewing, even though it may be much nicer than other homes on the street. You may have told your REALTOR® to “Bring me any offer. Frankly, I’d take less.” But compared to other houses for sale, your home simply looks too expensive to be considered.

If you price too low, you’ll short-change yourself. Your house will sell promptly, yes, but you may make less on the sale than if you had set a higher price and waited for a buyer who was willing to pay it.

TIP: Never say “asking” price, which implies you don’t expect to get it.

Price Against Comparable Sales in Your Neighborhood

No matter how attractive and polished your house, buyers will be comparing its price with everything else on the market.

Your best guide is a record of what the buying public has been willing to pay in the past few months for property in your neighborhood. Your REALTOR® can furnish data on sales figures for those comparable sales and analyze them to help you come up with a suggested listing price. The decision about how much to ask, though, is always yours.

Competitive Market Analysis (CMA): The list of comparable sales a REALTOR® brings to you, along with data about other houses in your neighborhood that are presently on the market, is used for a “Comparative Market Analysis” (CMA). To help in estimating a possible sales price for your house, the analysis will also include data on nearby houses that failed to sell in the past few months, along with their list prices.

A CMA differs from a formal appraisal in several ways. One major difference is that an appraisal will be based only on past sales. Also, an appraisal is done for a fee while the CMA is provided by your REALTOR® and may include properties currently listed for sale and those currently pending sale. For the average home sale, a CMA probably gives enough information to help you set a proper price.

Formal Written Appraisal: A formal written appraisal (which may cost a few hundred dollars) can be useful if you have unique property, if there hasn’t been much activity in your area recently, if co-owners disagree about price or if there is any other circumstance that makes it difficult to put a value on your home.

TIP: If you do order a market value appraisal, make it clear you don’t need an elaborate or full narrative report, i.e., the kind that’s complete with photos of the house and neighborhood. Floor plans and a site map is sufficient in most cases.

Market Conditions – Is it a Buyer’s Market or a Seller’s Market?

A CMA often includes a Days on the Market (DOM) value for each comparable house sold. When real estate is booming and prices are rising, houses may sell in a few days. Conversely, when the market slows down, average DOM can run into many months.

Your REALTOR® can tell you whether your area is currently in a buyer’s market or a seller’s market. In a seller’s market, you can price a bit beyond what you really expect, just to see what the reaction will be. In a buyer’s market, if you really need to sell promptly, offer an attractive bargain price.

If You Price High, Set a Schedule for Lowering the Price

Some sellers list at the rock-bottom price they’d really take, because they hate bargaining. Others add on thousands to the estimated market value “just to see what happens.” If you want to try that, and if you have the luxury of enough time to feel out the market, sit down with your REALTOR® and work out an advance schedule for lowering the price if need be.

If there haven’t been many prospects viewing your home after three weeks, you may need to lower your list price. If that doesn’t bring any prospective buyers, you may need to lower your list price again. Plan on doing that regularly until you find a level that attracts buyers. Make a written schedule in advance, before emotion takes over and you’re tempted to dig your heels in.

Offering Incentives to Hasten a Sale

Sometimes cash incentives are as effective as lowering the price, especially in the lower price range where buyers may be “cash poor.” You may offer to pay some or all of a buyer’s closing costs and discount points required by the buyer’s lending institution.

If you haven’t had much traffic through your house and you’re in a hurry to sell, you may want to add the offer of a bonus to the selling broker, in addition to their commission. An example of the wording for such an offer may be “to the broker who brings a successful offer before Christmas.”